{kind=link}

The Irish economy is expected to continue expanding at a robust pace in the coming years, according to a new report from AIB.

However, it states that this growth will be more moderate than the pace of recent years as the economy bounced back from the Covid-19 pandemic.

The inaugural AIB Economic Outlook Report forecasts that gross domestic product (GDP) will grow by 2.6% in 2025 and 2.4% in 2026.

Last year, GDP fell 3.2% due to a downturn in the pharmaceuticals sector.

The report states that Ireland’s industrial output and goods exports are expected to bounce back in 2024 and 2025.

Meanwhile, modified domestic demand (MDD), a less volatile gauge of domestic activity, is expected to grow by 2.4% next year and 2.6% in 2026.

This will be driven by a rise in consumer spending and in modified investment, the report states.

However, the report warns that a number of capacity constraints in Ireland in areas such as housing and transport could have a restraining impact on the economy.

We need your consent to load this rte-player contentWe use rte-player to manage extra content that can set cookies on your device and collect data about your activity. Please review their details and accept them to load the content.Manage Preferences

Inflation returns to normal range

According to today’s report, inflation has returned to the “normal” range and is expected to stay there in the near term.

“Irish inflation has been in rapid decline over the course of the past year as the sharp price rises in 2022 and 2023 drop out of the annual rate,” the report states.

It expects the annual harmonised index (HICP) of consumer prices to fall to 2.2% for 2024 from 5.2% last year, and to 1.9% and 2% in 2025 and 2026.

However, flash figures released by the CSO yesterday showed that the annual rate of inflation increased to 1.9% in May, up from 1.6% in April.

Speaking on Morning Ireland, David McNamara, Chief Economist at AIB, said there will be bumps in the road.

“I think the data from yesterday is interesting, and I think we will see that across the European Union,” he said.

“Energy price declines are starting to level off now, and there will probably be more bumps in the road ahead – but the drivers of inflation over the past few years have largely dissipated,” he added.

Robust growth in labour market

Since the beginning of 2020, employment has grown by nearly 340,000, or 14%, to a record high of 2.7 million people.

This compares to a trough of 1.87 million in 2012 post the global financial crisis.

The report states that unemployment is expected to remain close to the current low levels, with employment to top a record 2.8 million people by 2026.

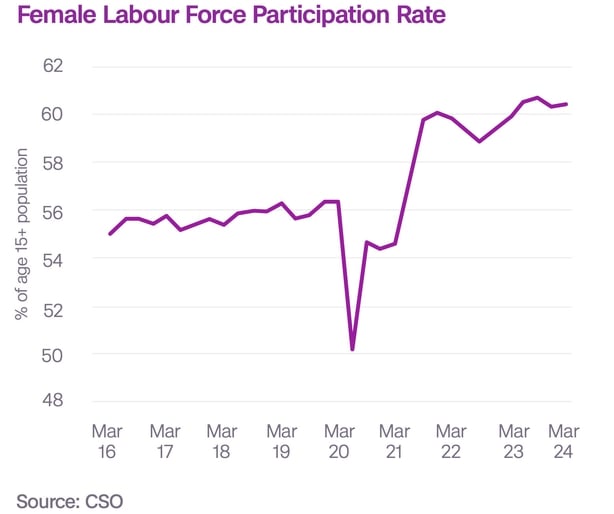

“This is as a result of strong population growth and the female participation rate surging since the pandemic, rising to 60.5% of the working age population in the first quarter of 2024 from 56.4% in the last quarter of 2019,” the report states.

It added that the introduction of flexible working since the pandemic may have driven the increase in female participation.

“However, there are signs this exceptional growth will cool as the labour market nears full capacity,” it states.

Impact of central bank rate cuts

Central banks have indicated that rate cuts are on the way, and the ECB is set to cut its base rate next week, with markets having factored in a further two cuts in 2024.

But, what comes next is still unknown.

“While there is some disagreement as to where exactly long-term interest rates will land, they are likely to be higher than the ultra-low rates of the 2010s,” the report states.

Mr McNamara said rates are likely to fall back towards 2-3%.

“It will be a gradual cut from here, so that is good news for the real economy and that will feed through to economic growth over a longer period of time,” he added.

There have been differing views globally in terms if the outlook for rate cuts this year, due to varying degrees of confidence that inflation is on a sustained downward trajectory in each of the economies.

The Bank of England has indicated that it could begin cutting during the summer.

However, the US Federal Reserve stated that rates will have to remain at current levels for longer than previously envisaged and may not cut until September 2024.

Global growth at historically weak levels

Global growth remains at historically weak levels, and is expected to remain so in the near term according to the IMF.

In this context, today’s report states that geopolitical risks could still knock some economies off course.

“The direct impacts are via higher commodity prices and supply chain disruption which could quickly feed through to higher inflation,” it added.

The main geopolitical risks which could spill over to economies, particularly in Europe, remain the war in Ukraine, alongside conflicts in the Middle East.